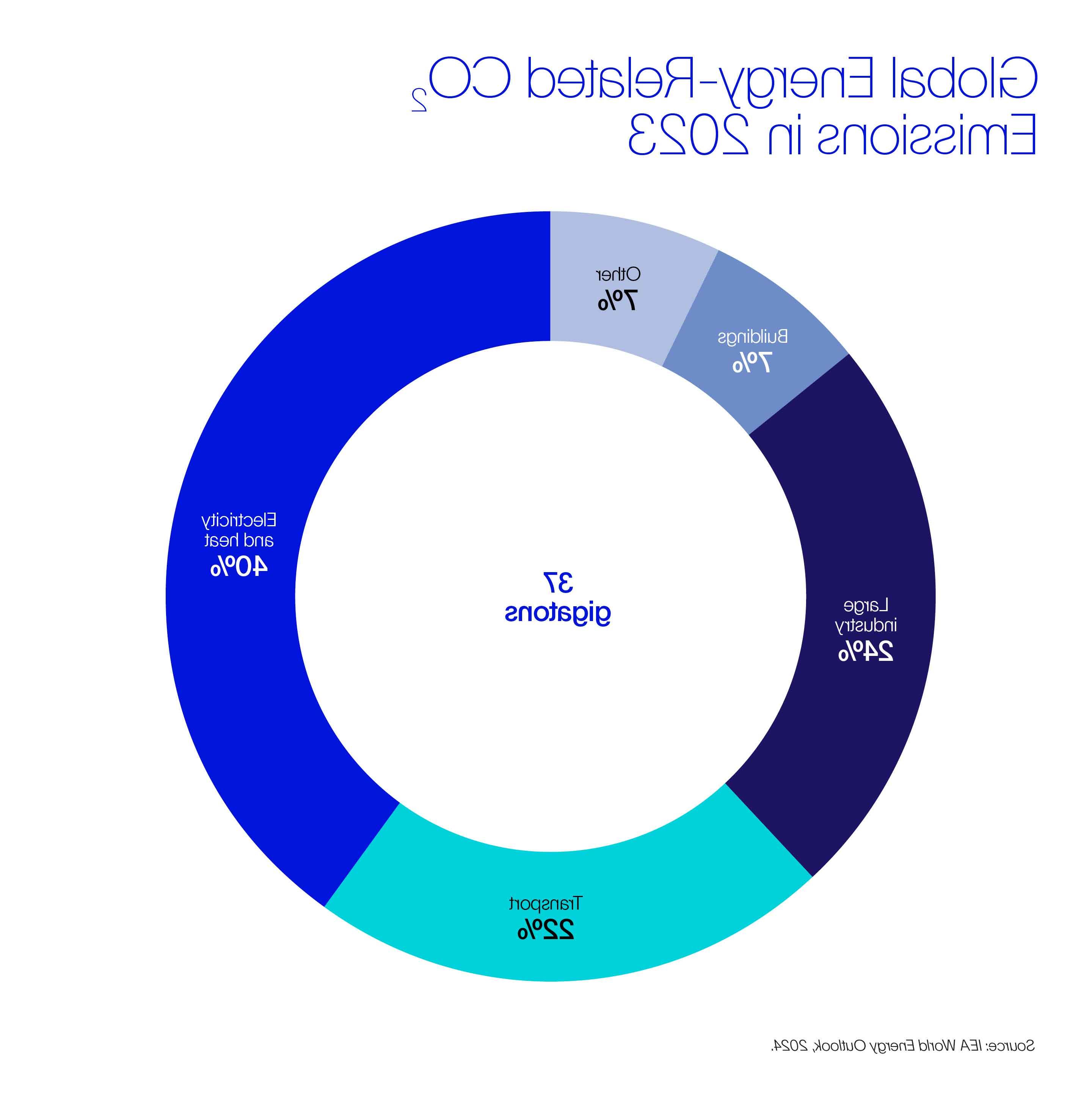

According to the International Energy Agency (IEA), the global energy system contributed 37 gigatons of carbon dioxide emissions in 2023. The predominant emitters—electricity and heat (accounting for 40% of energy-related emissions) and transport (accounting for 22%)—are seeing tremendous momentum, with investments beating projections each year. Decades of government support have enabled technological advancement, driving down the costs of key tech and making decarbonization solutions for both electricity and transport (think renewable energy sources and electric vehicles) economically viable. And they're moving at speed.

With line of sight on how to abate this “low-hanging fruit,” industrial decarbonization is the next critical focus.

Heavy industries make up 24% of global emissions, primarily driven by the production of iron and steel, cement, chemicals, and aluminum. But the basic requirements for decarbonizing these sectors are the same as those for decarbonizing electricity and transport. It requires that governments, businesses, and the public provide their support in creating economic conditions where technologies can incubate and scale.

The key factor, as always, remains time: How quickly can we accelerate the scale-up and adoption of the tech necessary to drive down these sectors’ emissions intensity? This is the challenge that must be addressed to push toward a lower-carbon future, not just for heavy industries but for the world.

Understanding the industrial decarbonization challenge

Industrial decarbonization poses a unique challenge in that many of these heavy industries are "hard-to-abate" sectors. This means that eliminating carbon emissions from their operations is inherently difficult due to the nature of their processes.

The industries in question typically produce two types of emissions: (1) energy-related emissions from power generation or fuel use and (2) process emissions inherent to their operations. Cement production, for example, requires heating limestone to isolate calcium oxide or "lime", which releases CO2. Similarly, the iron and steel industry relies on blast furnace or gas-based direct reduced iron (DRI), processes that emit significant amounts of CO2 during reduction.

While these industries can reduce their energy-related emissions by switching to a combination of renewable sources (when and where these types of energy source are available and financially feasible) and energy storage, that change only partially addresses their total emissions. Full decarbonization asks for innovative solutions that tackle both energy and process emissions, all without compromising productivity.

Key strategies for industrial decarbonization

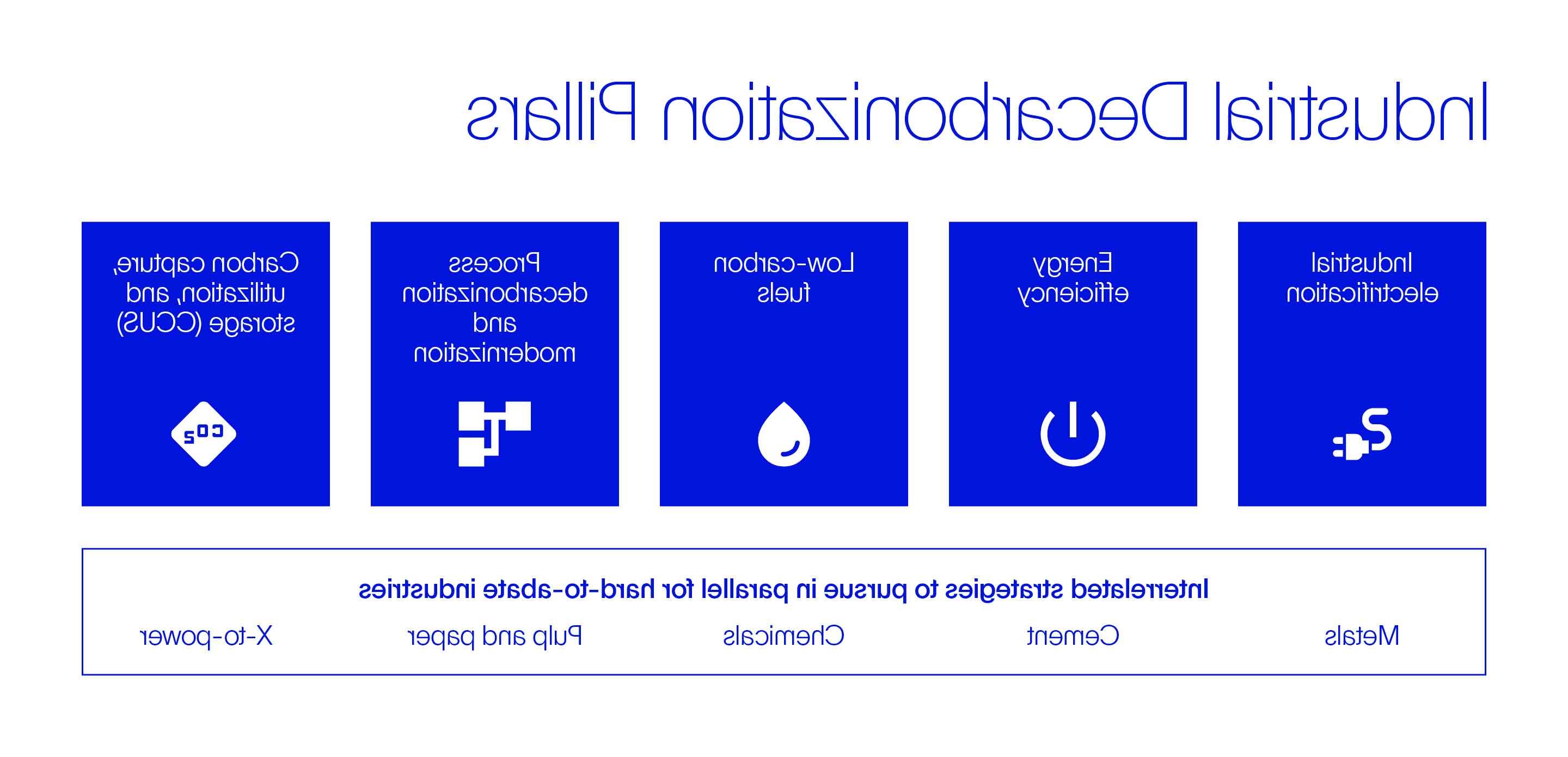

While there is no single solution, there are several strategies that hard-to-abate industries can and will continue adopting to reduce their carbon footprint.

- Industrial electrification—The process of replacing fossil fuel-powered industrial processes with electric ones.

- Energy efficiency—Improving energy efficiency is one of the simpler and, oftentimes, most cost-effective ways to reduce emissions. Heavy industries can upgrade their equipment, optimize their processes, and adopt energy-efficient tech to start.

- Fuel substitution—Switching to low-carbon fuel or renewable energy sources is another solid strategy. Replacing coal with natural gas or transitioning to low-carbon hydrogen as a fuel source are two good examples.

- Process decarbonization—Some industries need to make stronger shifts in their fundamental processes to achieve palpable emission reductions. Take the cement industry, once again: Manufacturers are currently exploring alternatives to limestone (e.g., calcined clays) that emit less CO2 during production.

- Carbon capture, utilization, and storage (CCUS): For industries where emissions are unavoidable or mature industries with significant existing infrastructure, CCUS offers a viable solution. This includes capturing the carbon at the point of emission and using or storing it in the subsurface (underground).

The challenges and opportunities in decarbonizing industry

While the strategies for decarbonization are clear, implementation remains more complex. Each industry faces its own challenges, meaning there’s no one-size-fits-all scenario; every sector requires solutions tailored to its needs. A couple of unique cases come to mind. The paper and pulp industry, for example, has made significant strides in its decarbonization journey, accelerating its progress by leveraging CCUS solutions. Same can be said about the waste-to-energy sector.

What’s important to note is that both of these industries benefit from the fact that CCUS could make them carbon negative. The biomass their processes use as raw material (trees, for example) have removed emissions from the atmosphere during their lifetime. So, capturing the carbon from these processes generates “high-quality” carbon credits, which—in turn—finance their decarbonization initiatives.

Similarly, the chemicals industry is starting to move, driven by government incentives across Europe and North America, investor pressure, market perception, and public demand for greener products. Meanwhile, you have industries such as cement or iron and steel that are still lagging due to the lack of incentives and regulatory support for funding their decarbonization.

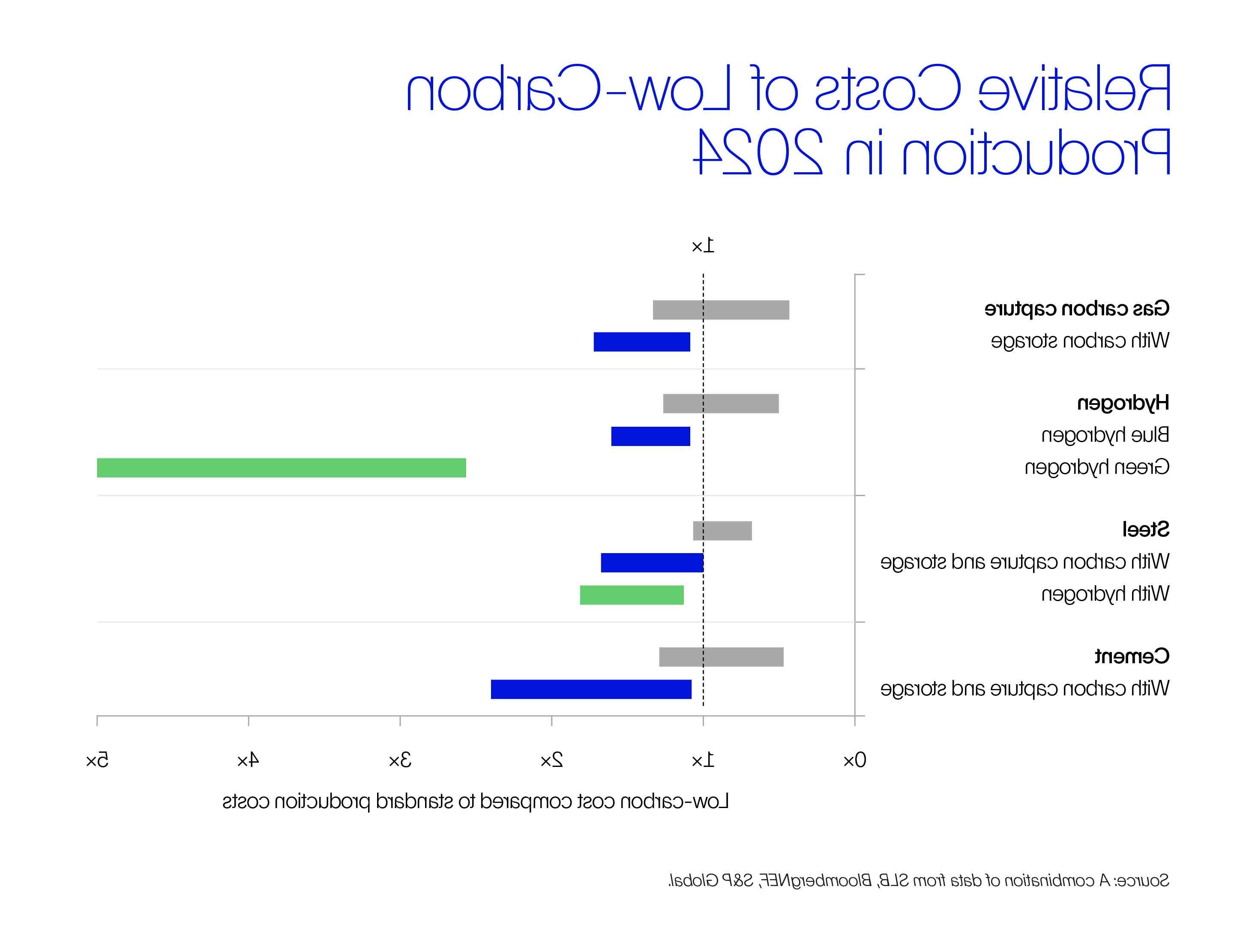

While the costs of new tech solutions may seem high today, they can be significantly reduced through learnings from the first few scaled projects. Achieving a tipping point for a decarbonized industry requires coordinated incentives and actions now to support the scaling up of these technologies, much like the decades of support that ultimately led the solar energy industry to its current techno-economic viability.

The cement industry globally could be perceived as moving slowly due to the limited availability of scalable decarbonization solutions. In Europe, however, more than 2 billion Euros’ worth of grants have been awarded to 11 plants, with announced projects covering more than 25% of the cement industry’s emissions. Cases like these demonstrate that markets respond when the right financial mechanisms are put in place.

The iron and steel industry is also exploring multiple pathways to decarbonization, including the use of CCUS, electric arc furnaces, and DRI plants that can switch to hydrogen in the future. While these are still early-stage technologies, they hold a lot of promise and potential for reducing emissions in the long term.

The role of financial mechanisms in industrial decarbonization

Financial mechanisms play a pivotal role in accelerating industrial decarbonization. This includes both "carrots” and “sticks,” referring to incentives and penalties, respectively. Regulations, such as the European Union's Emissions Trading System, establish a carbon market, with a cap on total emissions from various sectors. The market mechanism is set up so that, over time, the companies that emit more face financial penalties based on the amount of those emissions.

Conversely, incentives such as tax credits and subsidies encourage industries to adopt cleaner tech by offering economic rewards for reducing carbon emissions. The US has taken this approach with the Inflation Reduction Act, which mandates incentives for clean energy investment and production, low-carbon hydrogen production, and the capture and use of CO2

Consumers are also driving change by becoming increasingly aware of the carbon footprint of their purchases—and looking for ways to reduce it.

Businesses are responding, of course, by integrating sustainability into their core strategies and supply chains. Industrial decarbonization is no longer just a response to regulatory pressures, it’s now also a strategic move to meet the expectations of an environmentally conscious market and ensure a company’s long-term competitiveness and resilience.

Meanwhile, hyperscalers are willing to pay a premium for renewable energy to power their operations, as demonstrated by the kind of partnerships Google and Meta are making. These tech providers are keenly aware of their emissions impact and the role it might have on their customers’ choices. And so, they’re taking action.

Industrial decarbonization isn’t achieved in isolation

Successful industrial decarbonization requires that multiple stakeholders collaborate. Tech developers need to continue focusing on innovating the energy tech necessary to solve (in an economical and feasible fashion) the challenges of hard-to-abate industries. The heavy industries have a critical role to play as early adopters building or retrofitting to full-scale, lower-emissions plants. Governments and regulatory bodies are crucial in creating suitable incentives and frameworks that drive change. And finally, consumers have the power to demand greener products and services, thereby generating a market for low-carbon solutions.

Public-private partnerships (PPPs) among the various players are fundamental in accelerating the adoption of new decarbonizing tech. These collaborations provide the necessary funding, expertise, and infrastructure to develop and implement cutting-edge solutions. By pooling resources and sharing risks, PPPs can facilitate large-scale projects that might be too costly or complex for any single entity to undertake independently. Moreover, these partnerships can help bridge the gap between research and commercialization, ensuring that innovative tech moves from the lab to the market more swiftly.

The journey to industrial decarbonization may be complex, but it’s essential for achieving net-zero emissions. Each industry must identify the tailored approach that best balances its economic growth with environmental sustainability—there is no templatized solution and there is no one stakeholder that can do it all. But with the right strategies, tech, and financial mechanisms in place, heavy industries truly can continue to grow while reducing their carbon footprint. And that’s a fact.